Multivariate normal random draws.

Syntax: @rmvnorm(S[, n])

@rmvnormc(S[, n])

@rmvnormi(S[, n])

@rmvnormic(S[, n])

m: (optional) vector

S: sym, matrix

n: (optional) integer,

Return: vector, matrix

Draw random multivariate normals using the

density function.

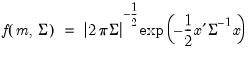

The multivariate normal density is given by

There are four different forms of the function, corresponding to different ways of specifying

. The forms are distinguished by different suffixes that are applied to the base “@rmvnorm” command and how they change the interpretation of the

S matrix argument:

@rmvnorm | “” | Supply  . |

@rmvnormc | “c” | Supply the Cholesky decomposition of  . This form is more efficient when performing multiple draws from the same distribution (compute the Cholesky once, but sample many times). |

@rmvnormi | “i” | Supply  . This form is more efficient than explicitly inverting  to supply  . |

@rmvnormic | “ic” | Supply the Cholesky decomposition of  . This form combines the efficiencies of the Cholesky and inverse forms. |

If the optional argument n is omitted, the function returns a vector containing a single draw from the distribution. If n is provided, n is the number of rows of the returned matrix, with each row representing a draw from the distribution.

Examples

= @dmvnorm(@identity(3))

returns a random draw from a trivariate normal distribution.

Cross-references