Panel Cointegration Testing

EViews provides a number of procedures for computing panel cointegration tests. The following tests are available in EViews: Pedroni (1999, 2004), Kao (1999) and Fisher-type test using Johansen’s test methodology (Maddala and Wu (1999)). The details of these tests are described in

“Panel Cointegration Details”.

To compute a panel cointegration test, select from the menu of an EViews group. You may use various options for specifying the trend specification, lag length selection and spectral estimation methods.

To illustrate, we perform a Pedroni panel cointegration test. The only modification from the default settings that we make is to select Automatic selection for lag length. Click on OK to accept the settings and perform the test.

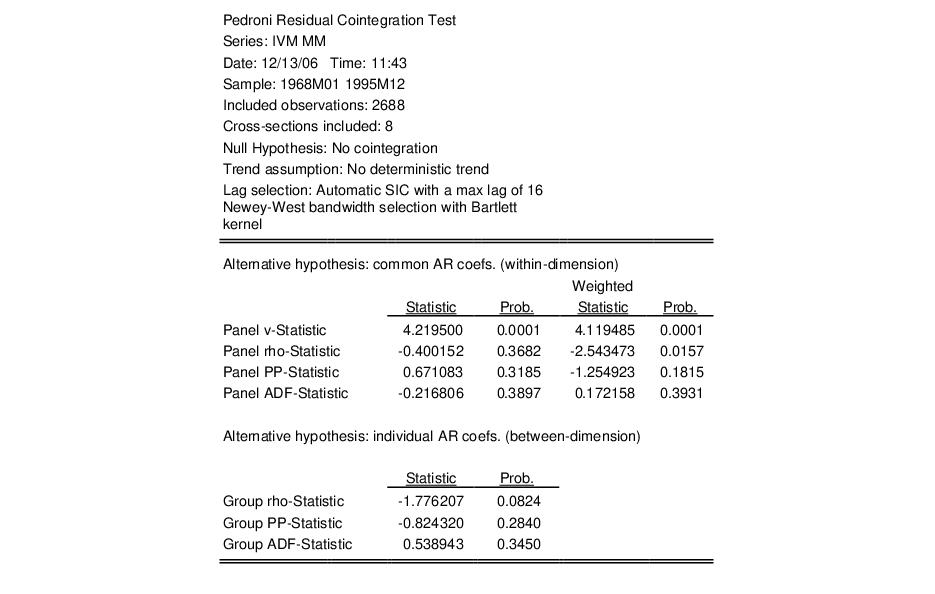

The top portion of the output indicates the type of test, null hypothesis, exogenous variables, and other test options. The next section provides several Pedroni panel cointegration test statistics which evaluate the null against both the homogeneous and the heterogeneous alternatives. In this case, eight of the eleven statistics do not reject the null hypothesis of no cointegration at the conventional size of 0.05.

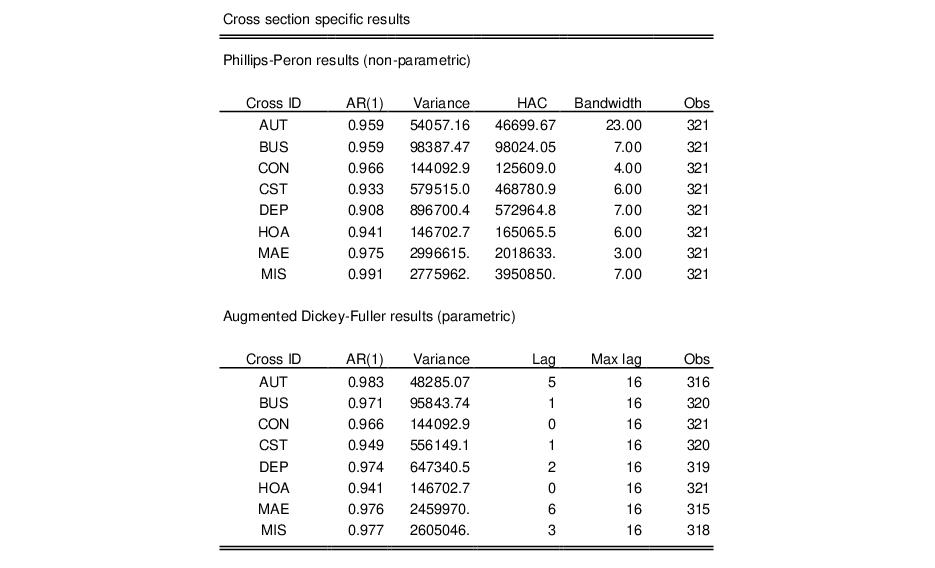

The bottom portion of the table reports auxiliary cross-section results showing intermediate calculating used in forming the statistics. For the Pedroni test this section is split into two sections. The first section contains the Phillips-Perron non-parametric results, and the second section presents the Augmented Dickey-Fuller parametric results.