EViews 12 New Features

EViews 12 New Econometrics and Statistics: Testing and Diagnostics

EViews 12 introduces a suite of new post-estimation diagnostics, as well as statistical tests and procedures:

- Impulse Response Enhancements

- Cross-Sectionally Dependent Panel Unit Root Tests

- Factor Selection Methods

- Wavelet Decompositions

- Elastic Net, Ridge and LASSO Enhancements

- GARCH Diagnostics

Impulse Response Enhancements

EViews 12 features a set of improvements for computing and displaying impulse responses and confidence intervals for VAR and VEC estimators.

- New impulse response user interface

- Bootstrap impulse response confidence intervals for both VAR and VECs

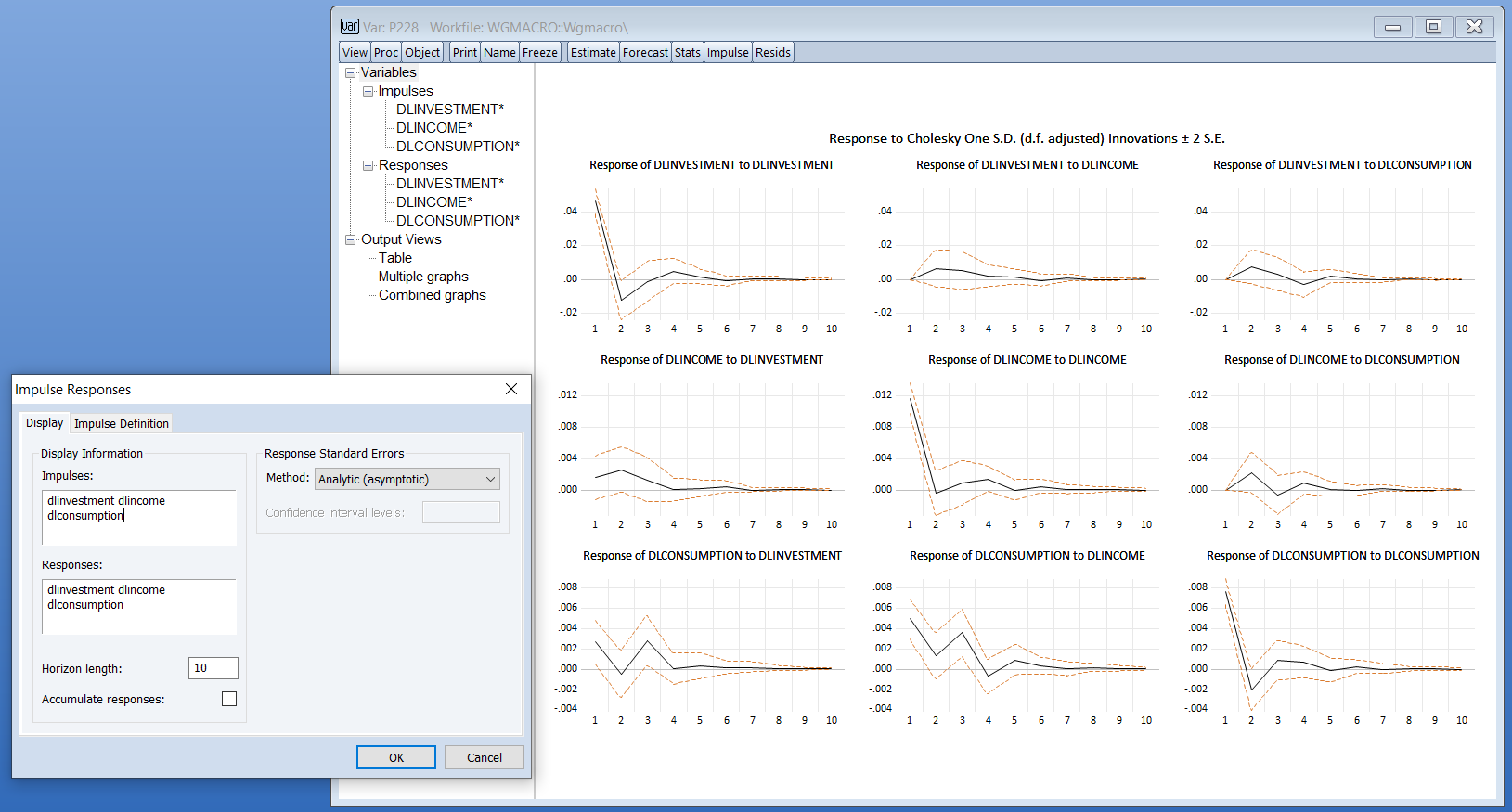

New Interface

The prior impulse response interface coupled the choices for which impulses and responses to display and the method in which they were displayed, with the various options for computing the impulse response and standard error. Thus, if a user first displayed a multiple graph of impulse responses and then wanted to show the results in a table, or perhaps display a subset of those original responses, the procedure would have to be respecified and recomputed from the beginning.

The new, dynamic EViews 12 interface allows for interactive selection of the impulse and responses to be displayed, as well as the method of display.

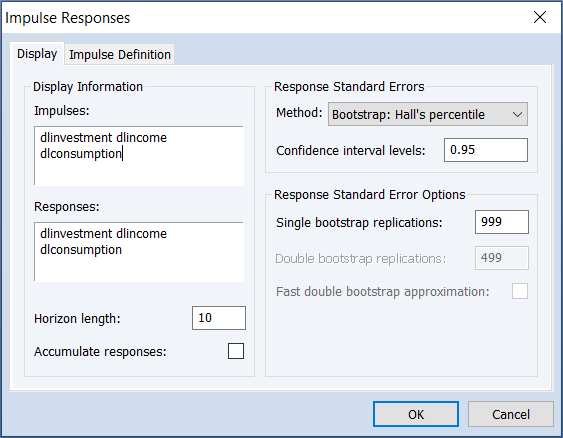

Bootstrap Confidence Intervals

EViews 12 introduces several new bootstrapping approaches to computing the confidence intervals for both VAR and VEC impulse responses.

These new tools allow you to compute residual bootstrap, residual double bootstrap, and fast residual double bootstrap estimates of these confidence intervals. EViews supports a variety of confidence interval bootstrap methods, including standard percentile, Hall’s (1992) percentile confidence intervals, Hall’s (1986) studentized confidence interval, and Killian’s (1998) unbiased confidence interval.

Cross-Sectionally Dependent Panel Unit Root Tests

Since many economic time series have short samples but are observed over many cross-sections, multivariate unit root tests that combine results for different cross-sections, colloquially referred to as first generation panel unit root tests, offered improved statistical power over their univariate counterparts. These first generation panel unit root tests involve unit root testing on pooled panel data, with (possibly) individual trend, intercepts, and lag coefficients. While this framework is a natural first step, it comes at the steep cost of requiring cross-sectional independence.

Tests which account for cross-sectional dependence have been termed second generation panel unit root tests. EViews current supports two important second generation contributions: Panel Analysis of Nonstationarity in Idiosyncratic and Common Components (PANIC) due to Bai and Ng (2004), and Cross-sectionally Augmented IPS (CIPS), developed by Pesaran (2007).

Factor Selection Methods

EViews 12 adds the Bai and Ng (2002) and Ahn and Horenstein (2013) methods for determining the number of factors to retain to our existing principal components and factor analysis engines, as well as the new cross-sectionally dependent panel unit root tests.

Wavelet Decompositions

Wavelet decomposition is a new Series view and procedure that can decompose a series into its long-run behavior (smooths) and short run behavior (details). Among other things, wavelets may be used to:

- Obtain a long-run approximation to a series by neglecting transient features (thresholding).

- Detect outliers.

- Decompose a series variance.

For more information, we have blog posts dedicated to the technical background as well as practical applications of wavelets.

Elastic Net, Ridge and LASSO Enhancements

Elastic Net (ENET) estimation, including the Ridge Regression and LASSO Estimation models, was added in EViews 11, and has proven a popular addition to the machine learning tools in EViews.

We have enhanced ENET in EViews 12 with the following features:

- Time series based cross-validation methods.

- New model selection views for displaying cross-validation results.

- Observation weights.

- Variable weights.

GARCH Diagnostics

GARCH models have been a fundamental part of the EViews estimation tool kit for over thirty years, and EViews 12 increases the toolkit by adding three new diagnostic views of GARCH models.

- New Impact Curve - plot the change in the conditional volatility against a change (or shock) in past news.

- Nyblom Stability Tests - a test of parameter stability or structural change.

- Engle and Ng Sign Bias Misspecification Tests - test for misspecification of the conditional variance model.