EViews 13 New Features

EViews 13 New Econometrics and Statistics: Testing and Diagnostics

EViews 13 introduces a suite of new post-estimation diagnostics, as well as statistical tests and procedures:

- Cointegration Testing Enhancements

- ARDL Diagnostics

- Pool Mean Group / Panel ARDL Diagnostics

- Enhanced Impulse Response Display

Cointegration Testing Enhancements

EViews 13 features improvements to Johansen cointegration testing, including:

- New deterministic trend settings

- Specification of exogenous variables as outside or inside (or both) the cointegrating equation

Deterministic trend settings

Deterministic cases in VEC estimation have been expanded to accommodate more control over restricting deterministics to appear among long-run coefficients. The set introduced in EViews 13 supports popular model configurations popularized by Lutkepohl (2005), in addition to the previously available configurations popularized by Johansen, Juselius and Hendry (2001) .

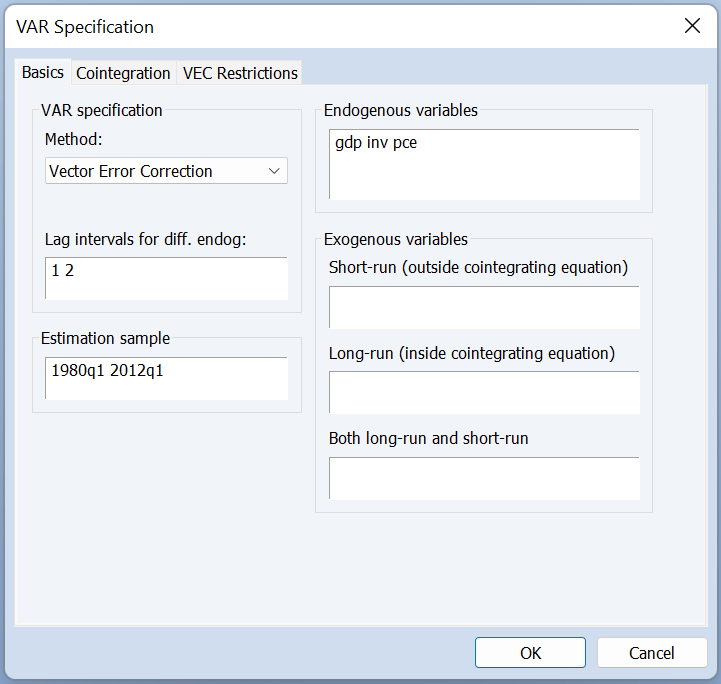

Exogenous Variable Specification

VEC exogenous variable specifications have been expanded in EViews 13 to accommodate the restriction of exogenous variables to the long-run coefficients only, short-run coefficients only, or both. Previous versions of EViews only allowed short-run coefficients. This expansion allows the exogenous variables to appear inside the cointegrating vector, and therefore influence cointegrating dynamics.

ARDL Diagnostics

EViews 13 introduces a new set of Auto-Regressive Distributed Lag (ARDL) model diagnostics.

- Enhanced results presentation

- Cumulative dynamic multiplier graphs

- Symmetry tests

EViews 13 offers enhanced presentation of ARDL results, with an clearer emphasis on high- lighting the error correction results and the cointegrating relationship.

The cumulative dynamic multiplier graphs show the cumulative marginal contribution of an explanatory variable to the dependent variable, and are used in the same way as impulse responses in VAR analysis.

As a addition to the non-linear ARDL estimation added in EViews 13, symmetry tests evaluate symmetry restrictions on the coefficients of the asymmetric long and short-run regressors

Pool Mean Group / Panel ARDL Diagnostics

EViews 13 also introduces a new set of Pool Mean Group (PMG) diagnostics.

- Cross-section bounds test for cointegration

- Similarity tests

- Symmetry tests

EViews 13 now performs Pesaran’s (2001) bounds tests for cointegration that are robust to whether variables of interest are I(0), I(1), or mutually cointegrated. These tests are for- mulated as standard F-test or Wald tests of parameter significance in the cointegrating rela- tionship of the Conditional Error Correction model for each cross-section.

Similarity tests are a Hausman test of the similarity of the PMG estimator to the mean-group (MG) and dynamic fixed effects (DFE) estimators.

Enhanced Impulse Response Display

EViews 13 offers considerably more control over the computation and display of impulse response (and variance decomposition) confidence intervals. You may now display multiple confidence intervals with user-specified sizes in a single graph, and employ shading to improve the visibility of these intervals.