EViews 11 New Features

EViews 11 New Econometrics and Statistics: Estimation

Improved Bayesian VAR Estimation

EViews 8 introduced Bayesian VARs to EViews, but due to their poularity, version 11 has completely reworked the calculation engine.

In particular, EViews now offers a choice of priors of:

- Litterman/Minnesota.

- Normal-flat.

- Normal-Wishart.

- Independent normal-Wishart.

- Sims-Zha.

- Giannone, Lenza and Primiceri.

All priors allow options for choice of initial covariance matrix calculation, and for the inclusion of the dummy observation priors.

The VAR forecasting and impulse response engines have also been expanded to allow for Bayesian sampling when performing these procedures from Bayesian VARs.

Mixed Frequency VARs

EViews 11 now supports estimation of mixed-frequency VARs using the Ghysels (2016) U-MIDAS and Bayesian estimation approaches.

With Bayesian mixed-frequency VAR estimation, the VAR forecasting and impulse response engines allow simulation through an MCMC algorthim.

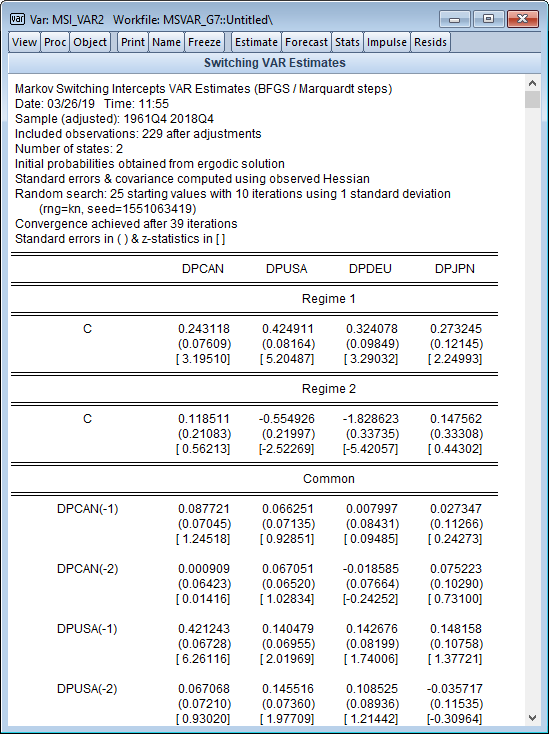

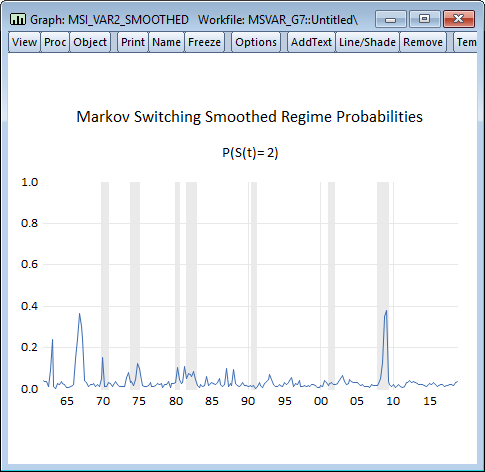

Switching VARs

Expanding upon the popular single equation simple and Markov switching models added in EViews 9, EViews 11 EViews 11 offers support for estimation of nonlinear VAR models where the nonlinearity is the result of simple and Markov switching.

Elastic Net and LASSO Regularization

Elastic net regularization is a popular solution to the overfitting problem, where a model fits training data well but does not generalize easily to new test data. Depending on the particular parameters chosen for the elastic net model, some or all of the regressors are preserved, but their magnitudes are reduced. Elastic net regularization is a branch of modern machine learning techniques used in econometrics.

EViews 11 includes tools for estimation of:

- Elastic nets.

- Ridge regression.

- LASSO models.

Functional Coefficients

EViews 11 offers the ability to estimate functional coefficient models, which are designed to handle shortcomings in traditional OLS and are natural extensions to classical non-parametric techniques.