EViews 9.5 New Features

EViews 9.5 New Econometrics and Statistics: Testing and Diagnostics

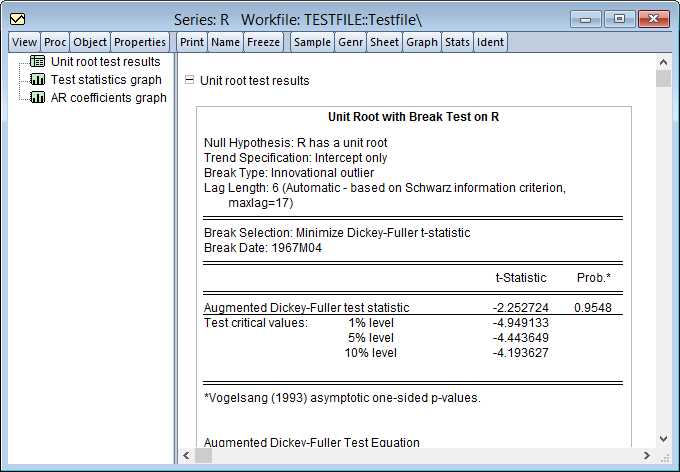

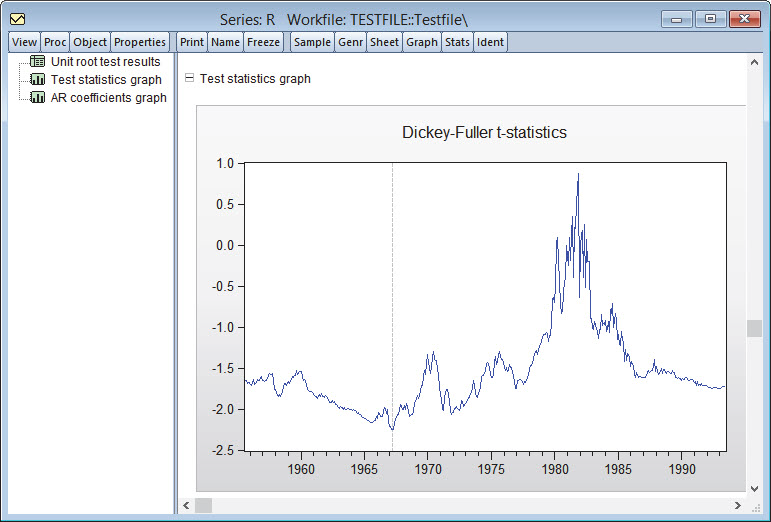

Unit Root Tests with a Breakpoint

EViews now supports the computation of modified Dickey-Fuller tests which allow for levels and trends that differ across a single break date. The framework follows the work of Perron (1989), Perron and Vogelsang (1992), Vogelsang and Perron (1998), Banerjee, et al. (1992).

EViews offers unit root tests with a single break where:

- The break occurs either slowly or immediately.

- The break consists of a level shift, a trend break, or both a shift and break.

- The break date is known, or unknown and estimated from the data.

- The data are non-trending or trending.

EViews will display the test results, and if the Display test and selection graphs checkbox is

selected, show all of the results in a spool

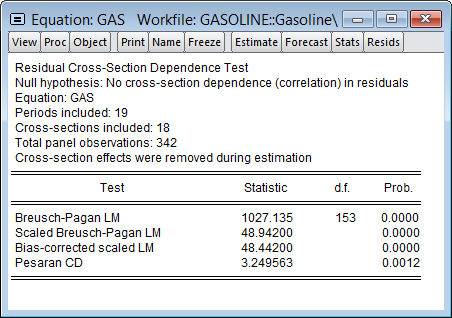

Cross–section Dependence Tests

EViews performs tests for cross-section dependence (CD) in panel data. You may perform the Breusch-Pagan LM (1980), Pesaran (2004) scaled LM and CD, and the Baltagi, Feng, and Kao (2012) bias-corrected scaled LM tests in panel and pool equation, and panel series settings.

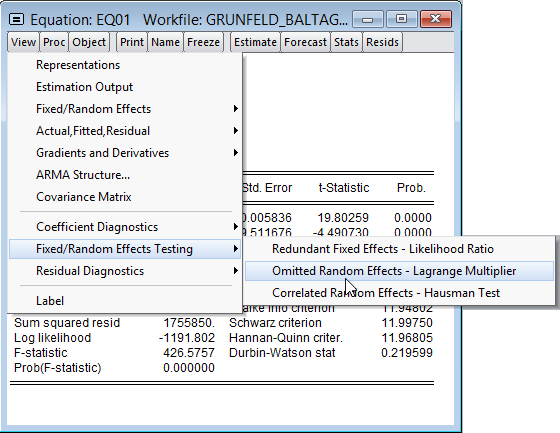

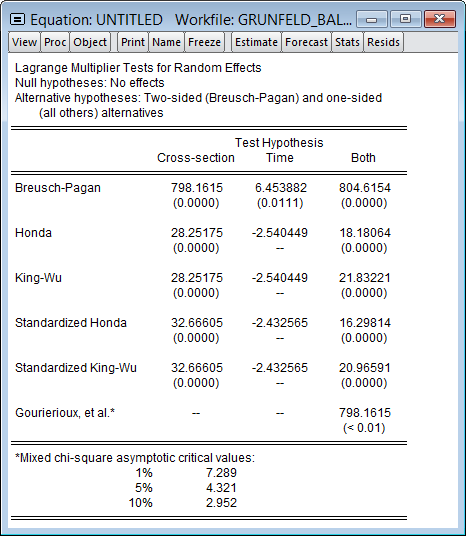

Panel Effects Tests

EViews allows you to test for individual and time unobserved random effects in a panel or pool equation. EViews computes the Breush-Pagan LM (1980), Baltagi and Li (199), Honda (1985), King and Wu (1997), Gourieroux, Holly, and Monfort (1982), Moulton and Randolph Standardized LM (1989) tests.